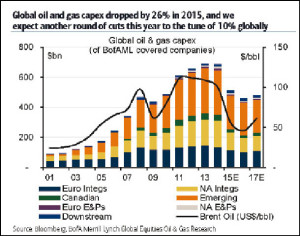

DOHA: Global oil and gas capital expenditures (Capex) dropped by 26 percent in 2015, and is expected another round of cuts this year to the tune of 10 percent globally.

Capex is a function of prices, and with prices recently below the $30/bbl mark, the actual 2016 cut is likely to end up larger than these expectations. In that respect, some companies have started to announce their 2016 plans and it seems that US producers are keen to cut as much or even more than last year, Bank of America Merril Lynch global energy report noted.

Continental Resources, Noble Energy and Hess just announced spending cuts of 63 percent, 49 percent and 41 percent, respectively, for this year compared with 2015. Meanwhile, non-Opec non-shale output should start to feel the pain in 2017, as the full investment cycle is around three to five years.

The research note said the list of the upcoming new projects has been already slimmed down, but current production from mature fields is also set to decline at higher rates as maintenance capex has been cut too. “Our analysis shows that decline rates increased significantly last year compared with 2013-14 levels. For example, UK decline rates accelerated from 9 percent in 2013 to 11 percent in 2015. The same story applies to other non-Opec countries such as Vietnam, Australia, Norway, Mexico and India. In contrast, decline rates in countries like Russia are holding up much better at this point, a trend that is likely to reverse, in our view, unless spending resumes. In aggregate, our weighted non-Opec production decline rate analysis suggests an average jump of nearly 0.6ppt, from 4.2 percent in 2014 to 4.8 percent in 2015, a level consistent with decline rates observed in 2008 and 2009. Net, total non-Opec supply is set to decrease to 56.4 million b/d in 2017 before rebounding to 57.5 million b/d in 2020, close to 2015 production levels.”

The report noted the structural shift toward a lower price environment will have profound and long-lasting consequences for non-cartelised production. With prices recently trading below the $30/bbl mark, BofA Merril Lynch’s expected 10 percent cut in 2016 global capex is starting to look modest.

Current production from mature fields is set to decline at higher rates as maintenance capex has been cut too. Net, BofA Merril Lynch now expect total non-Opec supply to decrease to 56.4 mn b/d in 2017 before rebounding to 57.5 mn b/d in 2020, near 2015 output levels.

The non-Opec conventional production now looks set to drop across the board by 2020, regardless of spot or forward prices. Shale may offer a silver lining, as the investment cycle is shorter than for conventional production. Given our expected upward price trajectory from here, the US rig count should increase again by 2H2016. As such, we see US shale output falling by 470 thousand b/d in a $40/bbl WTI environment, while growth returns at $50/bbl. Above $60/bbl, growth stands above 400 thousand b/d.