European economies are slowing

The International Monetary Fund has issued a fresh warning that Europe’s economy has weakened this year.

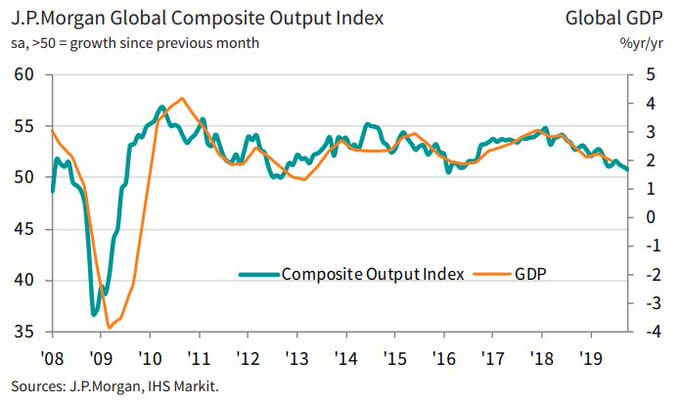

In its new Regional Economic Outlook for Europe, the IMF points out that growth has slowed this year.

That’s mainly due to weaker trade (thanks to the US-China tariffs), and a slowdown in factories this year. But there are now signs that the weakness is spreading…

The IMF says:

For most of the region, the slowdown remains externally driven. However, some signs of softer domestic demand have started to appear, especially in investment. Services and domestic consumption have been buoyant so far, but their resilience is tightly linked to labor market conditions, which, despite some easing, remain robust. Expansionary fiscal policy in many countries and looser financial conditions have also supported domestic demand.

On balance, Europe’s growth is projected to decline from 2.3% in 2018 to 1.% in 2019. A modest recovery is forecast for 2020, with growth reaching 1.8%, as global trade is expected to pick up and some economies recover from past stresses.

This echoes the message from the IMF’s Autumn Meeting last month, when it clashed growth forecasts for some European economies.

It only expects the eurozone to grow by 1.2% in 2019 (down from 1.3% previously), and by 1.4% in 2020 and 2021 (down from 1.5%).

The Fund also warns European leaders to prepare for the next crisis, and boost spending where they can, saying:

Countries with ample fiscal space should take measures to boost potential output, while countries with elevated debt and deficit levels should generally proceed with fiscal consolidation. This would also help address external imbalances.

Given elevated downside risks, contingency plans should be at the ready for implementation in case these risks materialize, not least because the scope for effective monetary policy action has diminished.

F