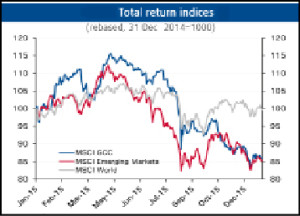

DOHA: GCC equities underperformed most international peers with the MSCI GCC total return index retreating 15 percent during the year, its weakest performance since 2008. The correction followed three years of solid performance. While regional markets fared worse than their international counterparts, equities in general were thrashed in 2015. Total GCC market capitalization stood at $904bn at year end, after shedding $200bn during 2015.

Oil prices and GCC equities have moved largely in tandem since oil prices started retreating in the second half of 2014. The relationship has been far from symmetrical, with correlations increasing notably whenever oil prices took a dive. With the exception of the large petrochemical sector in the Saudi stock market, GCC equities have little direct exposure to oil prices, though or course oil dependence pervades the GCC economies, NBK’s ‘GCC equity market’ update said.

While GCC government have expressed their commitment to support growth in the non-oil sector by sticking to their current development spending plans and maintaining large deficits in the medium term, a prolonged period of low oil prices could force governments to reduce capital spending and benefits, and could put pressure on liquidity. The issuance by the Saudi government of $28bn in bonds in 2015 to finance the fiscal deficit.

Markets in the region continued to be pressured by a number of domestic and market specific factors. In the UAE, worries about an imminent correction in property markets continued to make headlines. In Kuwait, with stock market liquidity remaining below historic averages and equities trading well below book value, several companies listed on the Kuwait Stock Exchange requested to delist, though the companies in question were all relatively small and had little impact on market capitalisation.

The GCC, though, saw some positive events. But these were largely overshadowed by volatility. In June 2015, Saudi Arabia opened up the market to direct foreign equity ownership, though only to qualified investors. Qatar also benefited from increased foreign investor interest with the upgrading in late Q3, 15 of the equity market to “Emerging Market” status by FTSE. In Kuwait, the CMA issued the final amendments to its bylaws late in the year, a step generally seen as a positive for the market.

All the GCC markets ended the year in red. Saudi Arabia and Dubai were the worst performers, down 17 percent each.

Despite a stellar performance earlier in the year, on the back of the decision to open up the market to foreign investors, Saudi equities were weighed down by further decline in oil prices. Dubai, with a larger foreign investor base, is typically more exposed to international factors, including oil prices. Qatar, Oman and Bahrain were each down 15 percent in 2015.

With banks now turning to fixed income markets to issue Basel III compliant perpetual and other bonds, and sovereigns also turning to capital markets to help finance their deficits, some liquidity is bound to be directed away from equities. Also, with regional rates now starting to rise following the first Fed hike late December, fixed-income assets are getting more attractive.