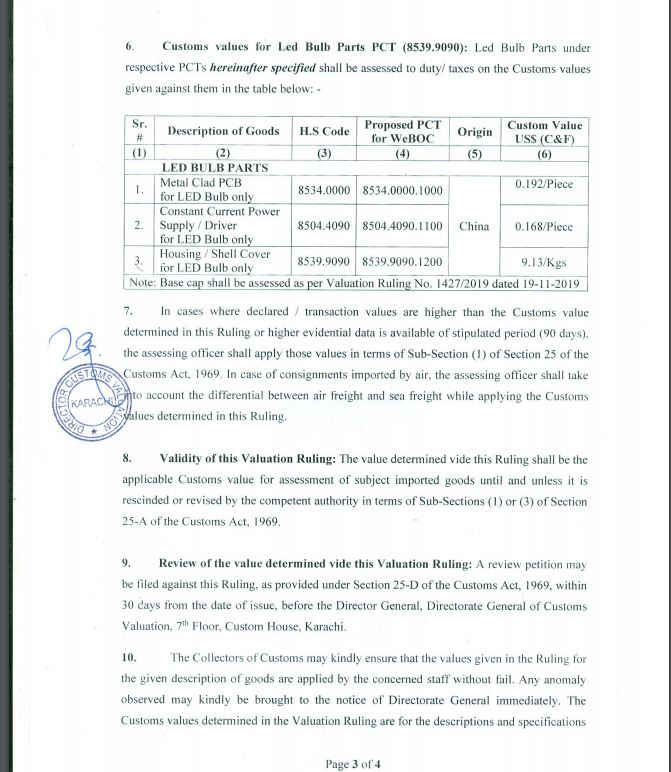

KARACHI: Directorate-General of Customs Valuation Director Shafiq Ahmad Latki has revised customs values of LED bulb parts vide valuation ruling no: 2915/2020 under section 25-A of the customs act, 1969. The customs values of LED bulb parts under respective PCT headings are determined as follows:-

Customs values of LED bulb parts were earlier determined through valuation ruling no. 1365/2019 dated 29.4.2019, Review applications were filed under section 25-D of the customs act, 1969 read with chapter IX of Customs rules, 2001 and the Director-General Customs Valuation while upholding the above valuation ruling observed, vide Order-in-Revision No. 16/2019 dated 21.10.2019, that the Director Customs Valuation may initiate working to determine the values of each parts and components in consultation with the stakeholders including the petitioners. Keeping in view the above facts, an exercise was initiated to re-determine the customs values of the subject goods under section 25-A of the Customs Act, 1969.

Meeting with stakeholders were convened on 11.12.2019 and 17.12.2019. The participants were requested to submit following documents before or during the course of meeting so that customs values could be determined:-

- Invoices of imports during last three months showing customs values.

- Websites, names and e-mail addresses of known foreign manufacturers of the item in question through which the actual current value can be ascertained.

- Copies of contacts made LCs opened during the last three months showing the value of item in question.

- Copies of sales tax invoices issued during the last four months showing the difference in price (excluding duty and taxes) to substantiate their contentions.

The representatives of manufacturers/assemblers namely, M/s Khyber Electric Lamps, M/s Elite Screener, M/s D.S. Technologies, M/s SAZ along with importers namely M/s Haadia Impax, M/s Light Concerns, M/s Osaka, M/s Electronic Office Products etc.

Customs valuation method given in section 25 of the customs act, 1969 were applied in sequential order to address the valuation issue at hand. Transaction values method under sub-section (I) of section 25 of the act ibid was found inapplicable because requisite information under the law was not available.